What causes interest rate rises to happen?

To understand the effects of an interest rate rise, first we will need to understand why it happens. There are several factors that lead to interest rate rise like:

-

- Inflation.

- Government borrowing.

- Demand for and supply of money.

The Reserve Bank of Australia (RBA) use monetary policy and fiscal policy for regulating economic activity.

A key role of the RBA is to conduct monetary policy to keep economic growth in check, achieve price stability, and manage economic fluctuations. Monetary policy involves the management of the money supply and interest rates by setting the target ‘cash rate’, which is the market interest rate on overnight loans between banks.

The RBA meets on the first Tuesday of every month to decide on the interest rate in Australia, and they either decide to lower it, increase it, or keep it the same.

The RBA’s Latest Meeting

The RBA has recently increased the interest rate on June 7, 2022 meeting in Australia by 0.50% the biggest cash rate hike in the last 22 years.

Earlier in the May 2022 meeting, the RBA increased the cash rate target by 0.25% after 11 years.

The consecutive increases have put the RBA cash rate or Australian interest rate now currently at 0.85%.

The inflation rate in Australia has increased significantly in the past year and extended periods of high inflation can lead to unemployment with business looking to cut cost. Unemployment is all time low now in Australia. It has dropped below 4% for the first time since the mid-1970s.

The main goal of the RBA for increasing the interest rates is aimed at employment, growth price stability, and economic prosperity and thus the welfare of the Australian people.

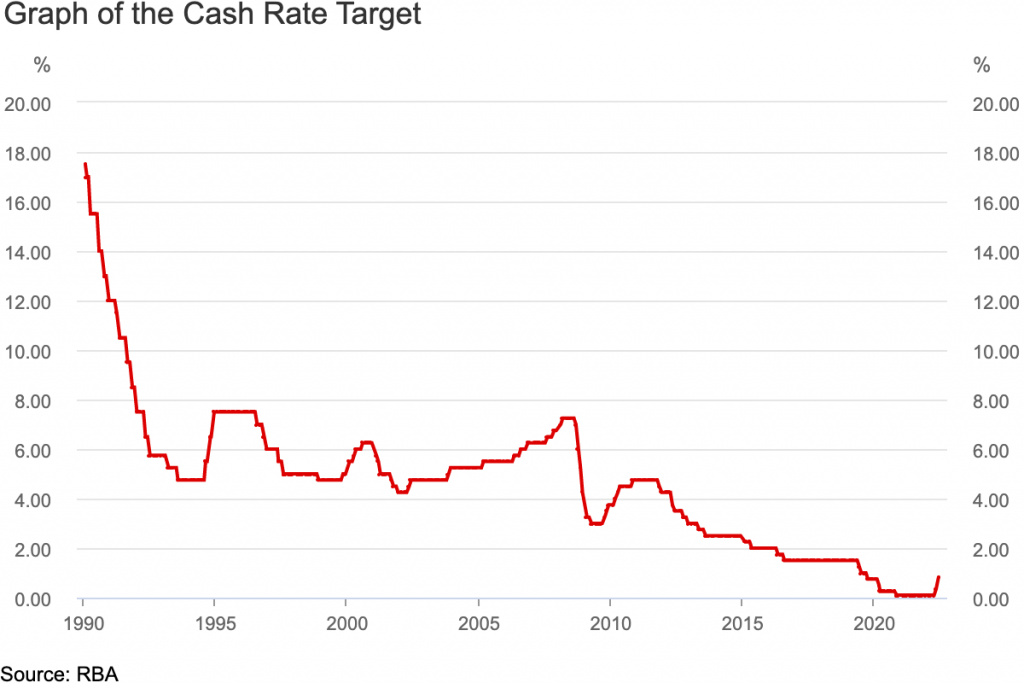

Here, is a graph of the cash rate target in Australia between 1990 and 2022. It gives an overview of the interest rate rise decisions taken by the RBA from 1990 till 2022.

How does the interest rate rise affect you?

The impact of the interest rate rise can have a diverse impact on people in general. To analyse the impact of the rate hike first we need to understand your position.

The interest rate rise has made living in Australia more expensive. For most Australians, a higher interest rate means that repayments on any kind of borrowing like mortgages, credit cards, and loans are more expensive. The impact of an interest rate rise on household budgets will have huge implications as most borrowers still have variable-rate mortgages in Australia.

On the other hand, a higher interest rate will lower inflation, boost employment, and will benefit both savers and non-homeowners in general.

With borrowing becoming expensive, there will be less demand for goods and services and people will look to spend less on non-essential things or will look to save.

To help you get a good idea of your expenses and savings feel free to use our Budget Planner and Savings Calculator. (All information is private and it’s free to use).

How does it affect the property market?

There was a steep hike in property prices since the beginning of the pandemic in 2020 with a national high of 35% in Australia. The rate at which property prices were increasing cannot go on even without an interest rate increase.

The average price of properties in Melbourne now is almost 1 million AUD after the sharp increase in property prices over two years. It had almost made it impossible for first home buyers to buy properties with a 10 percent deposit nearing $100,000 AUD. The interest rate rise is intended to stabilise the property market.

Normally when the interest rate goes up the property market cools down. However, as the property market made a steep increase over the last two years the prices are unlikely to fall significantly.

On the other hand, the increasing interest rate can be a boom in the rental property market as people’s affordability to buy houses will decrease. With decreasing affordability to buy houses, people will look for rental properties making it beneficial for investment property owners.

How does it affect you financially?

For homebuyers, the increase in interest rate means that their borrowing capacity has been reduced. With the decreasing affordability to buy a house, homebuyers may have to look for something cheaper.

On the contrary, an interest rate rise is beneficial for people with savings. If you are a homeowner without a mortgage and you have some deposits in the bank, then the interest rate rise is good news for you.

If you are looking at getting a mortgage or any kind of loan it will be more expensive.

If you have a fixed-term interest on your loan, then the interest rate will remain the same for you and the rate hike won’t affect you until your term ends.

If you are a lender the interest rate hike will be beneficial for you, but you have to factor in higher interest rates as well as other subsequent rises that are likely to increase before lending.

It is predicted that the RBA will increase the interest rate again soon. If the prediction comes true, that will lead to more increase in household repayments.

However, it is going to come as a bigger shock for borrowers who took out a fixed-rate mortgage during the pandemic when the interest rates were below 2.5%.

It is suggested to regularly review how the latest interest rates may affect your investments for making sure that you are on track with your investment strategy.

If you want to get more clarity on the pathway of your investment or looking for an experienced professional to guide you then call Aman Singh (Director) at 0412175700 from Credit Hub now. You can also talk to our team at 1300 782 944 or send us a note at info@credithub.codeforme.com.au.

Visit our Contacts page to see a range of ways we can get in touch with you.